Billionaires Who Never Were: FortunesLost to a Single Decision

A single signature, a rejected handshake, a moment of hesitation — some of the biggest fortunes in history were lost before they were ever made. These are the deals that didn't happen.

Opening

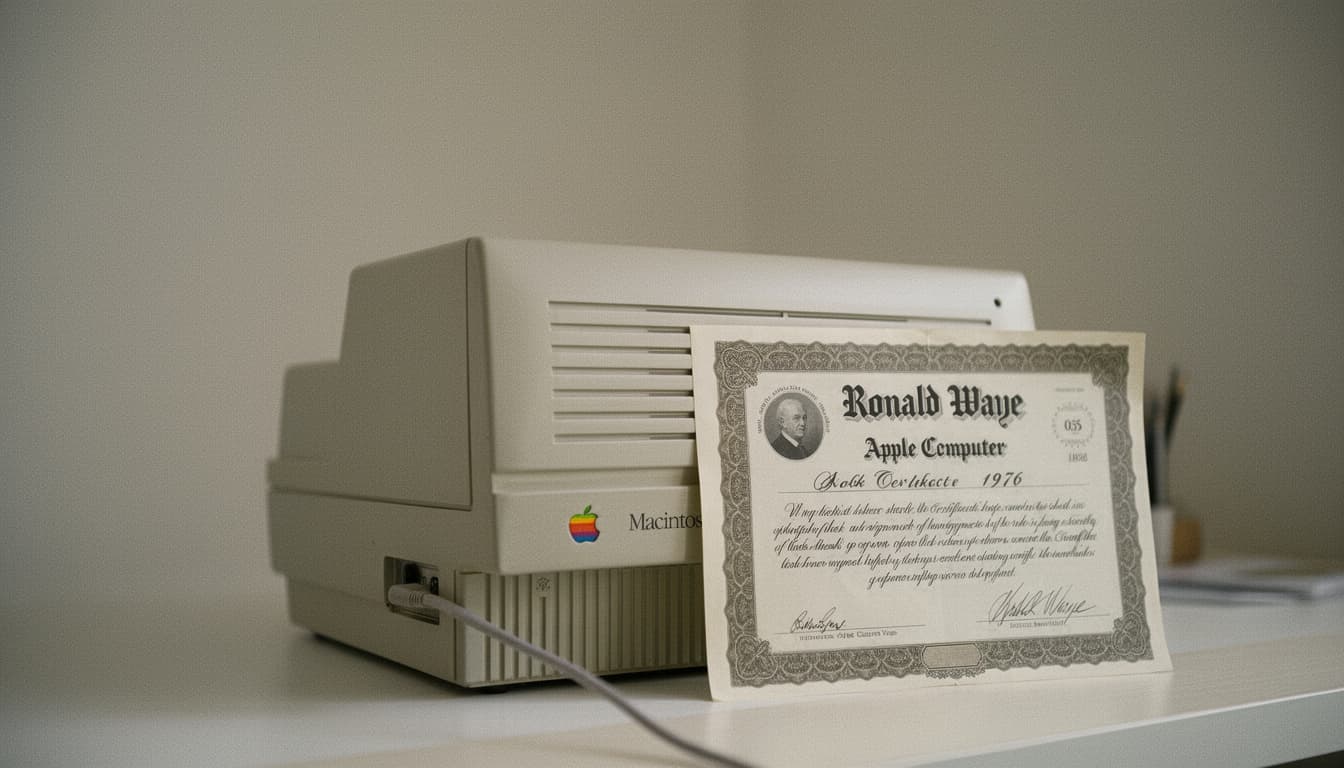

Most people know that Apple was founded by Steve Jobs and Steve Wozniak. What they don't know is there was a third co-founder who walked away from $300 billion.

Ronald Wayne owned ten per cent of Apple Computer when it was incorporated on 1 April 1976. Twelve days later, he sold his stake back for $800.

Wayne was the oldest of the three founders at forty-one. He'd been burned before by a failed business venture and was spooked by the personal liability that came with the partnership. Jobs and Wozniak were young and had nothing to lose. Wayne had a house and savings he couldn't afford to risk.

That decision cost him roughly $300 billion in today's money. Wayne spent his later years selling stamps and coins at a flea market in Pahrump, Nevada. He's said publicly that he doesn't regret the decision. Whether that's acceptance or just very expensive therapy is something only Wayne truly knows.

The best deals always look like the worst deals at the time they're available

The $50 Billion Microsoft Mistake

In 1979, Ross Perot was offered the chance to buy Microsoft outright. Bill Gates wanted somewhere between $40 million and $60 million for the entire company. Perot had built Electronic Data Systems into a billion-dollar enterprise, so the money wasn't the problem.

The sticking point was price. Perot thought Gates was asking for too much. Gates thought Perot was lowballing him. Neither man blinked. The deal died.

Gates went on to build the most valuable company in the world. Perot later admitted that walking away from Microsoft was one of his worst business decisions. Coming from a man who rarely admitted to mistakes of any kind, that's quite something.

The Most Expensive No in History

In 1999, Larry Page and Sergey Brin tried to sell Google to Excite for $1 million. Excite's CEO, George Bell, said no. Page and Brin reportedly came down to $750,000. Bell still said no.

The spread between $750,000 and Google's current market capitalisation makes this the most expensive no ever uttered

Excite was valued at billions at the time. Google was two graduate students with a better algorithm and no revenue model. Bell's reasoning wasn't irrational. Why buy unproven search technology when you already had one?

The algorithm wasn't just better. It was categorically different. Google would go on to become the most dominant information company in human history. Excite filed for bankruptcy in 2001.

The spread between $750,000 and Google's current market capitalisation of roughly $2 trillion makes this the most expensive "no" ever uttered in a business meeting.

The best deals always look like the worst deals at the time they're available

Blockbuster's Billion-Dollar Blindspot

In 2000, Reed Hastings and Marc Randolph flew to Dallas to offer Blockbuster a chance to buy Netflix for $50 million. Netflix was a struggling DVD-by-mail service losing money on every subscription.

The problem wasn't a lack of intelligence but a lack of imagination

John Antioco, Blockbuster's CEO, reportedly struggled not to laugh. His company had 9,000 stores, 65 million registered customers, and $6 billion in annual revenue. Netflix had a niche service and a website.

Antioco passed.

Blockbuster filed for bankruptcy in 2010. Netflix is now worth more than $250 billion. The difference between the two outcomes wasn't technology or capital or market conditions. It was the willingness to see where consumer behaviour was heading rather than where it currently sat.

When Yahoo Cut the Wrong Corner

In 2006, Yahoo offered to buy Facebook for $1 billion. Mark Zuckerberg was reportedly ready to accept. Facebook was growing fast but wasn't yet profitable, and a billion dollars was staggering for a company run by a twenty-two-year-old.

Then Yahoo's quarterly earnings came in below expectations. CEO Terry Semel cut the offer to $850 million.

Zuckerberg walked away. Not because $850 million was insufficient, but because the reduction signalled that Yahoo didn't truly understand what Facebook was building. Peter Thiel reportedly advised Zuckerberg that anyone who would cut $150 million from a deal over a bad quarter wasn't someone you wanted as an acquirer.

Facebook is now worth approximately $1.5 trillion. Yahoo was eventually sold to Verizon in 2017 for $4.5 billion.

The spread between $750,000 and Google's current market capitalisation makes this the most expensive no ever uttered

The Rational Mistake

Here's the thing: every one of these missed opportunities shares a common thread. The person saying no wasn't stupid. They weren't uninformed. In most cases, they were making what appeared to be the rational decision given the information available.

Wayne couldn't stomach the risk. Perot thought the price was wrong. Bell had a working product. Antioco had a dominant market position. Semel had a board demanding fiscal discipline.

The problem wasn't a lack of intelligence but a lack of imagination. Each decision was made inside a framework that assumed the future would look roughly like the present. That framework is almost always wrong when it comes to transformational businesses.

The companies that become worth hundreds of billions of dollars are precisely the ones that seem absurd at the point when they can still be bought cheaply. This is the paradox at the heart of venture investing: the best deals always look like the worst deals at the time they're available.

The Human Cost of Perfect Logic

The financial arithmetic of these decisions is staggering, but the human cost is subtler. Ronald Wayne is ninety years old and lives quietly in the Nevada desert. He's had to answer the same question for decades: "Do you regret it?"

Ross Perot went to his grave in 2019 knowing that the company he declined to buy had become worth more than a trillion dollars. George Bell has given very few interviews since Excite collapsed.

These aren't cautionary tales in the traditional sense. Nobody did anything wrong. Nobody broke the law or acted in bad faith. They simply misjudged the magnitude of what was in front of them.

And that's perhaps the most unsettling thing about these stories: not that the decisions were reckless, but that they were perfectly reasonable. The lesson isn't "say yes to everything." That's how you go bankrupt.

When something feels impossibly ambitious but the underlying logic is sound, the cost of saying no might be higher than you can calculate.

The problem wasn't a lack of intelligence but a lack of imagination

The best deals always look like the worst deals at the time they are available.

End of file

The next one drops Sunday at 7am.

One long-form story a week, plus the tools, frameworks and tactics I’m using to run my own media business. Written from the operator’s seat — not the consultant’s.

No threads. No spam. Reply anytime — I read every one.